April 2025 Market Update

The spring market is upon us. Higher Closed and Pending Sales numbers show a healthy, active market. Days on market was trending down and Sales Price/Final List price ratios above 100% (over 50% of the closed properties received list price or more) .

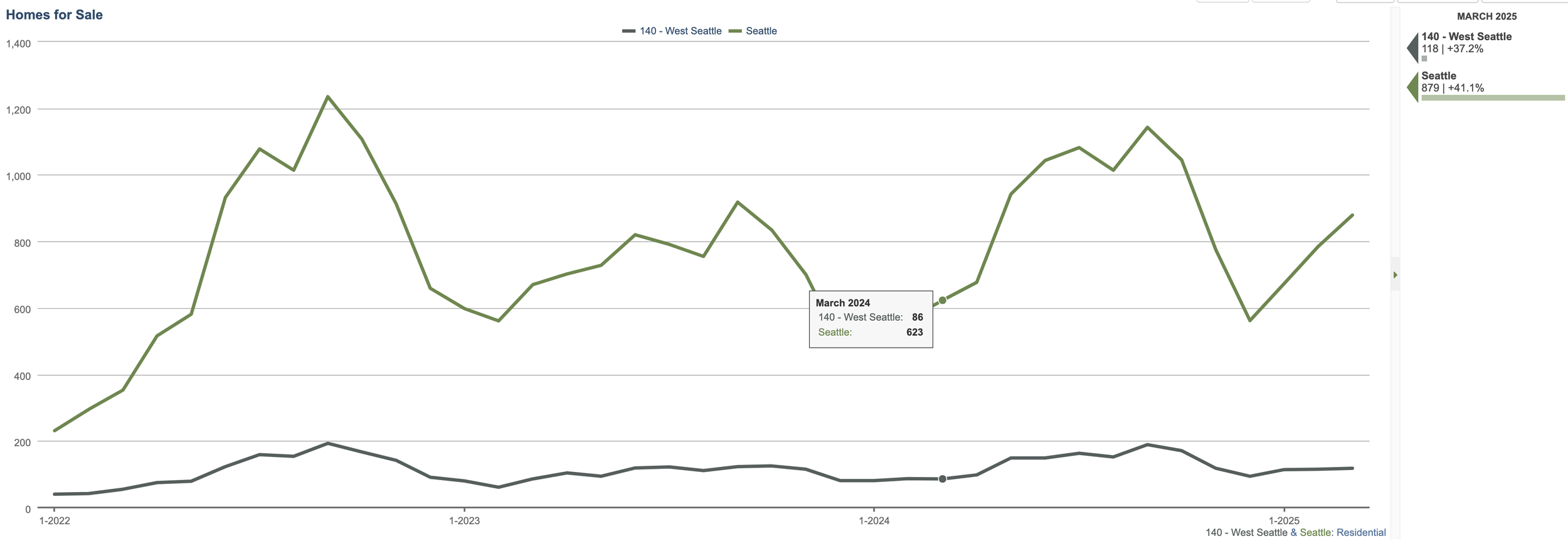

Inventory numbers might not look high (it’s basically the number taken at the end of the month) but we saw about 215 new listings (all properties) hit the market in March. We should expect that to rise as we get past Spring Break and into May. Sellers typically are able to get their homes market ready (with better weather in spring to paint and spruce up yard) and late spring calendars being more conducive to moving.

Median Pricing, however, saw a slight dip month-over-month. Is the market slowing down? We typically see less inventory and higher demand in the weeks between the Super Bowl up until Spring Break. This generally results in a rise in median price in the first couple of month of the year. Seattle Metro Median pricing increased but we saw a dip in month to month West Seattle pricing. What gives? We don’t feel the market is softening, as we are seeing and hearing of many competitive offer situations. Average Price was up last month, 961k in March compared to 935k in February. Median is typically a better indicator but might not tell the whole story for the month of March.

One month does not make a trend but there could be some reasons to why we saw this.

It could be the sale closed after the end of the month so would get figured in April numbers. There have been 18 closes the first week of April with a Median of 907k.

It might be the type of sale that closed. There might just have been more lower priced homes that closed in the month. There were quite a few New Construction townhome project sales that closed in March. Many of the sales had lower entry points so influenced the overall Median.

The below graph shows Median Price for Previously owned homes (doesn’t include New Construction Townhome/DADU).

West Seattle Median for Previously Owned homes was 837k vs. 805k for all Residential. Seattle metro PO homes were 1.017M vs. 990k for Res. Slight but important differences.

We’ll watch Median Price the next couple of months and see if something develops. We feel that there is a strong market for previously owned homes (especially turn-key) and the dip in Median wasn’t a true indicator of the WS market. But, there is a lot of economic uncertainty brewing. Definitely something to watch.

Inventory numbers followed historical trends and started a slow rise. Of note, there were 215 new listings (152 Previously owned properties and 64 New Construction) last month. Most of the inventory got absorbed by accepted offers. On average, there are about 120 homes on the market every week. Up from about 90 per week in the middle of the winter.

Typically we see more inventory hit the market towards the end of April into the summer months. April-July are typically higher inventory months. Last year, we saw 195 new listings (all property types) come out in April and 222 in May. It is hard to predict what will happen with this economic uncertainty but if more inventory does hit the market, it typically happens April-July.

Closed Sales were up last month. Some of these were properties were from properties going under contract in February. We would mention, lenders have been able to close properties in about 2 weeks so were are seeing quicker closes than traditionally (21-45 days). So properties receiving offers up until mid-March could close by end of the month. That’s fast!

Pending Homes indicate a pretty active month. We definitely saw more offer review day multiple offers and quite a few homes taking early offers (despite having listed review dates).

Seattle Metro followed historical norms with Rising Median, Pending, and Closed Sales. The market seems pretty competitive, especially for previously owned homes. This trend will likely continue until summer when inventory gains and demand wanes. Still, previously owned homes (especially better conditioned) should command a premium. Townhomes and new construction TH/ADU/DADU might get a bit saturated and have a smaller buyer pool. Older generation Townhomes seem to be doing well as there are only so many buyers for 2 Bed/1.5 bath, <1000sf townhomes. Especially when there are so many of them.

Interest rates have been fluctuating but have been trending down. 30 year fixed seem to be right around 6.5+/-%.